In this month’s update, we provide a snapshot of economic occurrences both nationally and from around the globe.

Key points:

– Ukraine exports start to flow which is hoped will dampen food price inflation globally

The Big Picture

The price of iceberg lettuce on the east coast of Australia just fell by 80% in a matter of weeks! Was this because the Reserve Bank of Australia (RBA) lifted its overnight borrowing rate from 0.1% to 1.85% this year with the prospect of more to come soon? No!

One doesn’t even need a high school education in economics to realise the iceberg problem was caused by extensive flooding and other adverse weather conditions in the east. Supply was crushed so farmers needed more per head for the smaller quantity they had to sell and some people were prepared to pay up to $13 a head for the privilege. For whatever reason, the supply of icebergs is back to normal – at least for the moment – and the price has returned to $2.49.

We are not trying to trivialise the current policies of various central banks but there is a strong parallel between this example and what some central bankers are saying.

Recently, the US Federal Reserve (Fed) chairman, Jerome Powell, made a strong statement at the annual global central bankers retreat at Jackson Hole, Wyoming. He went from being mild mannered earlier in August to a statement that pointed to the fact that ‘pain’ would be felt by many households and businesses as he kept increasing interest rates to rein in inflation and return it to within the 2% to 3% p.a. range. This, he said, was not a time to stop or pause the hiking cycle. Naturally, the S&P 500 on Wall Street fell over 3% that day and even further over the rest of the month!

We are not aware that the US has an iceberg lettuce problem but the world is suffering from high energy and general food prices partly caused by the Russian invasion of the Ukraine and supply-chain issues partly caused by China’s zero Covid policy.

None of these three supply disruptions will be cured by hiking interest rates. But there is a big difference between the price of lettuce and the price of food, energy or computer chips. Most, if not all households, can readily find a substitute for lettuce in their diets – or just forget about lettuce altogether. No one really needs to spend $13 on a lettuce! People around the globe are suffering big increases in energ¬y and food bills that they can’t afford and they can’t find a substitute for.

On top of the additional expenditure on fuel and food, any increases in interest rates – or holding them at high levels – to wait for general inflation levels to revert to normal causes corresponding hikes in mortgage and credit card repayments – and the cost of servicing business loans. That makes the pressure on the ability to pay for energy and food even greater.

What we have experienced in recent months are wild swings in economic data and a complete turnabout in the policy statements being issued by central banks. The 10-year bond rates in the US and Australia are going up and down in a wide range on these ‘news’ switches. That means households and businesses find it even harder to plan for what loans they can reasonably afford to take out – and that in turn affects the price of most goods and services and, in particular, housing.

To give a concrete example for Australia, at the start of August this year, the market was pricing in an RBA rate of 3.8% by the end of the year (from the then 1.35% rate) and a peak of 4.4% sometime during 2023. Just after the RBA board meeting on the first Tuesday of the month, the market priced in a reduced peak of only 3%. At the end of August, after the Jackson Hole meeting, that peak was raised back up to 4% from 3%. So, what should potential mortgagees and business owners do and what are the implications for investors?

Quite possibly, prudent, risk-averse people would allow for a higher rate than might or might not happen – or even being contemplated by the RBA behind closed doors – which means demand for housing goes down more than it needs and with it house prices. It is a commonly held view that falling equity in residential property from households not actually trading in property puts a dampener on their other retail expenditures.

As it happens, data on Australian retail sales for July just came in very strongly at +1.3% when only +0.3% had been expected. Also, for July, the unemployment rate even fell to a ‘tiny’ 3.4%. What will the changes in central bank ‘jawboning’ do to actual sales and unemployment during and after the August swings in sentiment? We can’t be sure but it is very unlikely that such behaviour by central bankers is helping to smooth the economic cycle.

Let’s also look at some relevant facts. And facts are relatively sparse in these debates. Unsubstantiated opinion counts for little. The Fed’s preferred measure of inflation is known as “core PCE”. Core refers to the fact that volatile energy and food price inflation is excluded from the calculation. PCE stands for Personal Consumption Expenditure. There is also a headline rate that does not exclude the volatile components. On top of that there are the core and headline CPI inflation results to which many other countries mostly relate.

The US usually relies on annual data for GDP growth and inflation that compares the current underlying figure for the level of GDP or the CPI with the corresponding period 12 months before. That means it takes 12 months for a big change in GDP or prices to work its way through the calculations. Of course, the US also produces monthly estimates for inflation and quarterly estimates for economic growth that do not suffer the overhang problem but these more regular data points are more likely to jump about a bit when underlying growth or inflation are not changing much.

As it happened, on the morning of Powell’s Jackson Hole speech, the PCE measures of inflation were released – only hours before he spoke – so he should have known that the latest headline monthly read was actually 0.0% and the core read was +0.1%. Hardly the stuff to inspire panic. Indeed, it is not possible to get a much better read as deflation (indicated by these numbers being negative) is, perhaps, even more scary than inflation!

Earlier in August the CPI reads came in. The headline monthly read was 0.0% and the core read was +0.5%. So, of the eight numbers produced on inflation each month, the Fed focuses on the big scary annual figures that include the overhang and not the benign monthly numbers we just quoted. And the month before (June) the statistics weren’t bad either – but not quite as good. There is building evidence that the worst of inflation may be behind us but it is not (yet) the time to celebrate its demise.

It’s not just the traditional measures of inflation that are giving us some hope. It was reported that US freight prices – one of the supply-chain issues fuelling general inflation because of a shortage of truck drivers amongst other factors – were up +28% on the year but actually down 2% on the month. And monthly house prices are down for the first time in three years. The Case-Shiller index is up 18% on the year but down 0.8% on the month.

So, from a monetary policy perspective we believe that central bankers are in general terms viewing their world, inflation and their respective economies through the following lens:

“All price inflation hurts all households but they (central bankers) cannot control all prices. Some increases are from so-called supply shocks such as the China chip shortage, the Russia energy supply rationing and the Ukraine grain export blockages. But those price increases, as well as some from other sources, are causing some ‘demand-side’ pressure through local wage increases and the like.

They will do what is needed to bring down demand-side inflation with interest rate policies but, after deciding what amount of inflation cannot yet be controlled, they will ease off this policy measure before they cause unnecessary damage to the economy.

Since households are hurt by prices that are higher from whatever source, governments need to be mindful of the upward pressure this in turn puts on wages. They cannot afford policy that leads to a wage price spiral, such as that which existed in the 1970s and 1980s when wage expectations fed off price increases that circled back into price rises”

At the latest report we have seen, 30 ships had left the Ukraine’s Black Sea ports loaded with grain and have made it to safe harbours in Turkey and beyond. The plan is apparently to increase this flow to 100 ships per month. If this occurs it should take some pressure off food prices – not just grain but, say, egg prices as they rely on the price of grain to feed the chickens.

Since 40% of Germany’s energy comes from Russia it will find a hard time trying to side-step that issue. But in the UK, which also has had major energy price surges, the incoming replacement for Boris Johnson is considering reversing some of the green initiatives regarding reliance on fossil fuel. It is all very well to want to switch to renewable energy but not until sufficient clean energy is available. There is a long, cold winter ahead and little tolerance for those who stopped all fossil fuel developments.

Despite the implications we here in Australia, the US and developed Europe are having in relation to inflation and interest rates, in other parts of the world the same situations exist but the effects and the policy responses are amplified significantly.

For example, Argentina has its cash rate at 69.5% and inflation is at 74%. On the other hand, Turkey has inflation running at 80% but it just cut its reserve rate from 14% to 13%. Japan, which glided through the 1970s and 1980s when most of the world suffered from stagflation (slow or negative economic growth and high inflation) without pursuing tight monetary policy is doing it again.

The Bank of Japan was again on hold in August; it is not falling into the trap of pushing up rates because that is the global trend!

Australian Equities

During the first half of August, the ASX 200 continued the stellar run which began in July. Then, along with the S&P 500 and comments from the Fed, our index plunged sharply, recovered back to its August peak and the fell again to finish just about flat for the month.

The Energy and Materials sectors were the clear leaders in August. The Financials and Property sectors were among the worst performers most likely on the back of interest rate outlooks and property prices.

Although our earnings season is ‘on’ it hasn’t been grabbing the usual attention as bond market movements have taken centre stage. Our analysis of Refinitiv broker-forecasts indicate that capital gains prospects for the next 12 months are now a little softer than average but it is too soon to draw a strong conclusion. Brokers take different amounts of time to update their forecasts and company reports are spread out over many weeks.

International Equities

The S&P 500 also extended its July run well into August but it faltered as the Fed raised rates, gave a hawkish outlook, and then finished August with Jerome Powell’s Jackson Hole speech.

The VIX ‘fear gauge’ almost returned to its normal operating range at the start of the month but rose sharply at the end of August.

Until we see how the Fed performs at its next meeting on September 21, it is hard to see there being any clear direction for Wall Street.

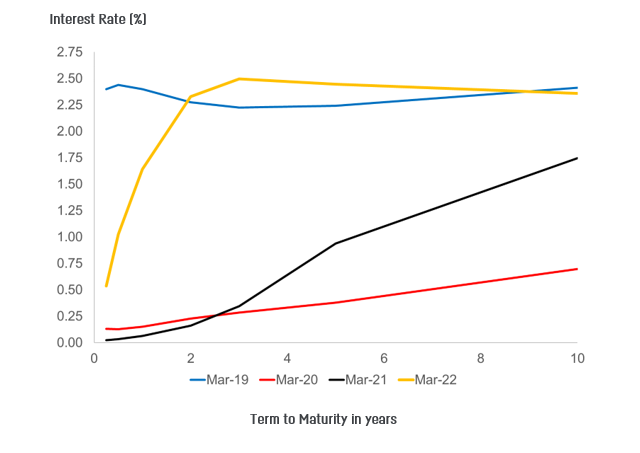

Bonds and Interest Rates

The Reserve Bank of Australia (RBA) again lifted its overnight borrowing rate by 50 bps this time to 1.85%. Other central banks including the Fed, the Bank of England (BoE) and the Reserve Bank of New Zealand (RBNZ) also lifted rates but, interestingly, the Bank of Japan was on hold at the last meeting and the Bank of Turkey actually cut its rate from 14% to 13% even though its inflation is running at 80%.

It is clear to many – not just us – that many central banks are implementing strategies that do not fully recognise that much of the inflation problems is the result of supply-side issues.

The CME Fedwatch tool, which is a standard when it comes to estimating what the market is pricing in for Fed rate hikes, had, until recently, a stable probability of there being a 50 bps or 75 bps hike in September with the latter being a bit more likely at 60%. The Jackson Hole speech by Powell on ‘pain’ from rate hikes has taken that latter probability to more like 72%.

We believe that unless central banks soon pause their interest rate hiking strategies, an economic recession may well follow.

Other Assets

Australia

For the first time in 2022, there were some mixed signals in the labour force data. The unemployment rate fell to 3.4% which is the lowest since the early seventies. But July witnessed the first fall in total employment this year – and it was by a sizable 40,900 jobs. On its own, there should be no alarm for one bad employment result from this small sample survey – but we will keep an eye on it next month. The total number of hours worked fell by 0.8%.

On the wages front, Australia recorded an annual increase of 2.6% including a 0.7% increase for the quarter. While that sits well with the long-term average, the latest CPI inflation read was 6.1% eclipsing the nominal wages read. Workers fell behind by 3.5% (= 2.6% – 6.1%) over the year in so-called real terms. That is the extent of the cost-of-living crisis.

The big data surprise for the month was the beat in retail sales. A rise of +0.3% was expected but the outcome for July was +1.3% and that is well ahead of what might be thought of as a monthly inflation read (Australia does not publish monthly inflation data like the US).

China

China is highly unlikely to get anywhere near producing the official expectation for economic growth of 5.5% this year.

Retail sales limped across the line at 2.7% against an expected 5.0%. Industrial production fared a little better at 3.8% against the 3.9% of the previous month – but 4.6% had been expected. It is unusual for China data to miss expectations by so much.

Nancy Pelosi, the Speaker of the US House of Representatives, made an unusual visit to Taiwan at such a sensitive time. There were no scheduled official meetings but it drew the ire of China. Just before she departed the island, China flew 25 fighter jets over the area.

Since China is yet to abandon its zero-Covid policy, it is hard to see the supply chain issues – particularly around chips for cars and other machines – easing materially any time soon.

US

The US posted a massive nonfarm payrolls jobs number. 528,000 new jobs were created in July and the unemployment rate was again a very low 3.5%. The strength of this number caused the market to incorporate tighter monetary policy and so another month for share prices got off to a bad start.

The Inflation Reduction Act finally got passed into law. It is a policy concerning climate change, health care and taxation. It doesn’t seem to say a lot about inflation except in the name of the bill.

It has taken a long time for Biden to get his pet project through Congress. In the process, his approval rating has plummeted and the mid-term elections on the 8th of November are looming large.

A recent survey reported by the New York Times, found that only 17% of the population approves of the direction Biden is taking. A massive 77% disapprove of the direction in which the US is heading. That is a lot of unhappy people in a country of 330 million.

With a slim majority in the lower house and the Senate controlled by the casting vote of the Vice President, there is talk reported of needing a new Democratic candidate in two years to stand for President.

The US is also facing a new phase in its post-GFC recovery. From now, QT – or quantitative tightening – starts in earnest. QE – or quantitative easing – undoubtedly helped the economic recovery by lowering longer-term interest rates and increasing liquidity. After a period of pausing the bond buy-back policy, QT is getting underway by removing $95 bn per month from the government debt of $9 trillion. It is uncharted territory but we all probably remember the taper tantrums when QE was first eased – and now it is now being reversed!

We are arguing that there are some nascent signs of a recovery in US inflation. Retail sales came in flat for the month in line with expectations. Sales, excluding autos were up by 0.4% for the month possibly reflecting the chip shortage. There is a shortage of new cars forcing up the price of used cars.

Europe

The debate between the two candidates vying to replace Boris Johnson as PM have each flagged reversing some of its green policies. While it is laudable to want clean energy and a zero-carbon footprint, it makes little sense if people can’t afford the energy for heating and cooking.

The Bank of England (BoE) is forecasting inflation of 13.1% for October and the latest reading of 10.1% is the largest number in over 40 years. Interestingly, the BoE is predicting inflation returning to 2% by 2025. Perhaps they know something about Russia’s plans than we don’t.

Rest of the World